If you have ever stared at a red screen, felt your heart pounding in your chest, and stubbornly refused to close a losing position because you just knew it was going to bounce back—you are not alone. And more importantly, you are not stupid.

You are simply fighting a losing battle against millions of years of human evolution.

The democratization of financial markets has given everyday investors unprecedented access to complex instruments and zero-commission trading. But this access has exposed a critical vulnerability: our biological hardware was not designed to process financial probability.

When you strip away the charts and the candlestick patterns, trading is ultimately an exercise in neuroeconomics. If you want to survive the markets, you have to understand the invisible biological forces actively sabotaging your portfolio.

The Invisible Triggers: How Weather Alters Your Wealth

You might think your trading decisions are based purely on technical analysis or corporate earnings. But what if I told you that your profitability today might depend on whether or not you needed a jacket during your morning commute?

It sounds absurd, but academic research proves human trading intuition is shockingly fragile. A recent behavioral finance study analyzing high-frequency transaction data found that variables as irrelevant as morning weather and ambient air temperature dramatically alter cognitive function and baseline mood.

Researchers discovered that on warmer-than-median mornings (specifically between 8:00 AM and 9:00 AM), traders experience natural mood repair. Their cognitive function improves, and they make more rational decisions. However, on colder-than-median mornings, traders' behavioral biases inflate by a staggering 28%.

This isn't just a retail problem. Massive institutional investors have been shown to display a significantly higher propensity to purchase equities on sunny days, whereas extensive cloud cover reliably depresses market participation. If your risk management strategy can be derailed by a cloudy Tuesday, you don't have a strategy—you have a mood ring.

The "Win It Back" Loop and The Disposition Effect

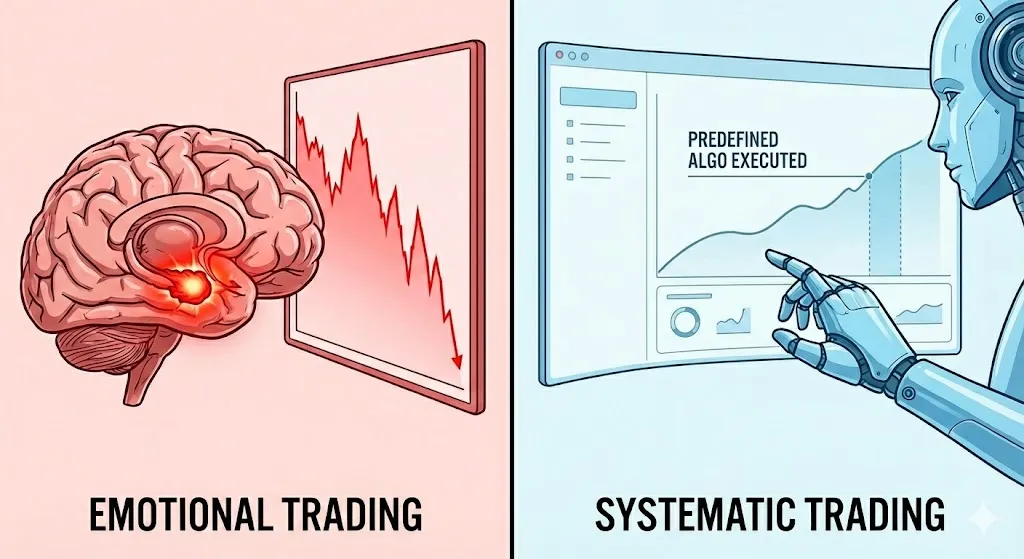

The most destructive force in any trader's career is a psychological phenomenon known as the Disposition Effect. Rooted heavily in prospect theory, it describes our irrational tendency to realize gains prematurely to secure a psychological "win," while simultaneously holding onto losing positions to avoid the emotional pain of a loss.

Let's look at the math. When researchers compared professional human day-traders to algorithmic trading systems in volatile markets, the results were sobering.

Human professionals realized 28% of their available gains, but only 17% of their available losses. This mathematical asymmetry guarantees a skewed risk-to-reward ratio that slowly bleeds a portfolio dry. Why do we do this? Psychologists call it realization utility. Booking a small profit acts as a pleasant mood-repair technique, while clicking "sell" at a loss inflicts acute, literal emotional pain.

This pain frequently triggers the "revenge trading" loop. The brain momentarily conflates a financial drawdown with a physical survival threat. The internal monologue rationalizes, "Yes, I am emotional, but this specific setup looks highly profitable." By the time the trader realizes they have abandoned their statistical edge for an emotional reaction, their account is often liquidated.

Algorithms, on the other hand, operating in the exact same market conditions, realize gains at 34% and losses at 33%. They exhibit virtually zero disposition effect because machines don't have egos to protect.

How to Build an Architecture of Rationality

The intersection of behavioral economics and physiological data reveals a harsh truth: discretionary, gut-driven trading is a trap. To survive, you must abandon intuition and adopt the posture of a systems engineer.

Here are three research-backed ways to systematize your trading and mitigate your emotional biases:

1. Short-Circuit the Amygdala with Defined Risk

Human beings are fundamentally loss-averse. When you buy a regular stock, your theoretical downside is 100% of your capital. This unbounded risk acts as a continuous psychological stressor.

Consider the story of a retail trader named Sarah. During a volatile earnings season, Sarah bought shares of a high-flying tech company, fully intending to sell if it dropped 5%. When the stock unexpectedly gapped down 15% at the market open, her amygdala hijacked her logic. Instead of cutting her losses, she froze. Hoping it would bounce back, she watched the stock bleed out another 20% over the next week before finally capitulating at a devastating loss.

You must cap your risk mathematically before the trade is ever placed. You can do this using two primary tools:

-

Stop-Loss Orders: This is an automated ticket resting with your broker to sell a position immediately if the price drops below a specific, predetermined level. It cuts the cord automatically, removing your finger from the button when panic sets in.

-

Vertical Option Spreads: For more advanced traders, this involves simultaneously buying and selling options contracts at different strike prices. Because you are collecting premium on one side and paying it on the other, your maximum possible loss is strictly capped at the net cost of the trade. Even if the stock goes to zero, you cannot lose a penny more than your predefined limit.

When the maximum loss is a binary, fully accepted cost of doing business, you eliminate the "deer in the headlights" panic response.

2. Stop Anchoring to the Past

Your brain desperately seeks reference points to estimate value. Retail investors persistently anchor to a stock's 52-week high, assuming a stock that has fallen significantly is inherently "cheap" or "due for a rebound."

Take Marcus, an amateur investor who bought into a popular electric vehicle manufacturer at $200 a share. When the broader market pulled back and the stock fell to $150, Marcus anchored to his initial purchase price. His thesis wasn't based on the company's current valuation or momentum; his entire strategy became "waiting until it gets back to break-even." He held the stock for two years of underperformance, tying up capital that could have been deployed into new, winning setups.

Sophisticated corporate insiders systematically exploit this bias. Stop looking at where a stock used to be. Base your exits and entries on current, unfolding market geometry—like probabilistic moving averages and dynamic volatility bands—rather than an emotionally salient, arbitrary historical price tag.

3. Run a "Premortem" Exercise

Elite quantitative teams utilize a behavioral mitigation technique developed by cognitive psychologist Dr. Gary Klein called the premortem.

Unlike a post-mortem (analyzing what went wrong after your capital is gone), a premortem happens before you execute a trade. Imagine a proprietary trading desk in Chicago preparing to launch a new algorithm. Before writing a single line of live code, the team lead walks into the room and says: "It is six months from now. Our strategy has failed spectacularly, and we have lost 30% of our fund. What went wrong?"

The team is then forced to list every possible structural, market, and execution flaw that could have led to this hypothetical disaster. Research shows that this exercise of "prospective hindsight" increases your ability to identify future risks by 30%. It bypasses the ego's defense mechanisms and forces you to view your strategy with brutal objectivity before capital is on the line.

Treat Losses as Data

The ultimate goal of systematizing your trading is a profound paradigm shift. In a discretionary framework, a loss is a personal failure. In an engineering framework, a loss is simply an expected data point within a vast, pre-calculated statistical distribution.

When you know mathematically that your system has an edge, a string of losses is no longer a reason to abandon your strategy in a blind panic. It is just the math playing out. Here is how you practically turn losses into data:

-

Log Trades in Batches of 20: Stop evaluating your success on a trade-by-trade basis. A single trade is statistically meaningless noise. Commit to executing a specific strategy 20 times in a row exactly as planned. Only after the 20th trade do you review the aggregate win rate and profitability.

-

Track the "R-Multiple" (Risk Multiple): Instead of tracking dollars, track multiples of your risk. If you risk $100 on a trade (1R) and make $300, you made +3R. If you lose, you lost -1R. Normalizing your data this way detaches your ego from the dollar amount and focuses your mind on the efficiency of the system.

-

Tag Your Emotional State: Keep a physical or digital trading journal. Next to your entry price and stop loss, add a column for "Emotional State at Entry" (e.g., Anxious, Bored, FOMO, Confident). Over a 90-day period, you will generate hard data showing exactly which emotions correlate with your largest drawdowns.

Stop trying to predict the unpredictable. Build your rules, automate your risk, and let the math do the heavy lifting.

Comments are disabled.